How Biotiful became the UK's biggest kefir brand and was sold to Müller for £115M

A former Russian figure skater bootstrapped Biotiful Gut Health for 13 years, hit £46.8M revenue with 70% UK kefir market share, and timed her exit last year at peak growth.

Welcome to The Food Stack, a weekly newsletter about investing in the future of food. Written by Vincent Kuiper, founder of Gota Ventures, an international angel syndicate investing in seed-stage European foodtech and consumer brands.

Contents

The Setup: in 2016 the Dragons rejected Biotiful as uninvestable. In 2021 Müller tried to build the same category internally and failed. In 2025 Müller paid £115M for the company the Dragons had passed on.

Why This Category / Why Now: how kefir went from unknown UK product to £100M+ category in a decade, and why the strategic acquirers are circling.

The Winner’s Playbook: the seven moves that took Biotiful from one founder in West Sussex to a 70% UK market share at exit, including the £4M share buyback that locked in the founder’s full upside.

How Others Are Playing It: The Collective and Lifeway, two functional dairy comparators that show why cap table cleanliness might matter more than revenue scale.

What Went Wrong (or: The Risks): why 70% market share commands only ~2.5x revenue, the structural ceiling on dairy multiples, and the post-acquisition execution risk.

Is There Room for New Entrants: where the next functional dairy winner might come from, and three specific gaps in continental Europe.

Takeaways: what founders and investors should remember.

The Setup

Please watch this video, it makes the story even more fascinating. Huge respect to Natasha

In 2016, Natasha Bowes walked into Dragons’ Den asking for £250K at a £2.5M valuation. Four of the five Dragons passed. Peter Jones told her she had made herself “uninvestable” and called her valuation “ridiculous”.

Deborah Meaden called even a 50% discount to that valuation “crazy” and was the only one who made an offer: 45% equity for £250K investment.

Natasha looked strong, determined, and rejected.

Nine years later, Müller paid £115M for her kefir brand, while Natasha still owned 100% of the company at signing.

Müller is the German dairy giant behind Müller Rice, Müllerlight, and Müller Corner, with operations across the UK at scale (Market Drayton, Telford, and Yew Tree Dairy among them). Biotiful is the London-based kefir brand that, in the year ending March 2025, generated £46.8M in revenue with £4.8M of pre-tax profit, on the back of 44% revenue growth and 111% profit growth in a single year. The company sells a range of kefir products, such as kefir drinks, shots, yoghurts, high protein drinks, and more recently also ‘gut health meal boosters’. By the time the deal closed, Biotiful held approximately 70% of the UK kefir category.

Founder Natasha Bowes with a selection of Biotiful products

This is the deal I have been most curious to pull apart since the gut health M&A wave started landing. A few things make it sit differently from the other UK functional food acquisitions of the past 18 months. First, the financial data is the cleanest of any deal in the queue. Companies House filings published in December 2025 give us a fully audited picture of FY2025 just months after the deal closed. Second, the founder kept majority control of the cap table all the way through to exit, then bought out the remaining minority holders in a £4M share repurchase 12 months before the deal. That is not how most CPG founders structure their journey, and it is worth understanding why.

What I find most interesting about Biotiful is the gap between how the brand is usually described and what the numbers actually show. Biotiful is sometimes positioned in the press as the British kefir success story, with Natasha Bowes as the founder who turned a niche Russian fermented drink into a £100M+ category. Müller paid £115M for a brand at the exact peak of its standalone growth curve.

Bowes had built a cap table that let her capture nearly all of the upside. All details I found out point to a founder whose instinct and discipline served her at the right moment.

I want to walk through this one because there is a sharper investor lesson here than the headline number suggests, and because I think it changes how European founders should think about the trade-off between bootstrapping and venture capital in functional food.

Why This Category / Why Now

UK kefir is a category that did not exist commercially before Biotiful launched in 2012. By the time Müller acquired the brand in April 2025, the category was worth roughly £100M at retail and growing in double digits in both volume and pricing terms (per Kantar). This is the structural backdrop for the deal, and three numbers anchor it.

First, kefir specifically. The UK kefir category has grown from effectively zero in 2018 to nearly £100M in retail value by 2024 (per Bowes, citing Nielsen data). Biotiful holds roughly 70% of that category. The Collective, which was acquired by Yeo Valley in March 2025, holds another meaningful slice through its kefir-yogurt range. The remaining share is split across smaller challengers and own-label products. This is a tightly concentrated category at the leadership end, and a fragmented one at the tail.

Second, the broader functional dairy space. The UK functional yogurt and dairy drinks segment was estimated at over £400M in 2024 by IRI/Circana. Probiotic and gut-supporting products are the fastest-growing subsegment. Globally, the digestive health products market is now valued at roughly $116.92B and growing at 8.74% per year (Precedence Research, cited in FoodNavigator). The European gut health supplements segment alone is projected to grow from $4.35B in 2024 to $8.15B by 2033, a 7.1% CAGR. Functional dairy sits inside this broader macro trend and benefits directly from it.

Source: Lifeway

Third, the M&A cadence has accelerated. In the past 24 months, the UK gut health and functional food M&A wave has produced four meaningful transactions: Hero Group’s acquisition of Deliciously Ella (September 2024, estimated £40M+), Yeo Valley’s acquisition of The Collective (March 2025, undisclosed but on £26.6M turnover), Müller’s acquisition of Biotiful (April 2025, £115M), and Hero Group’s acquisition of The Gut Stuff (April 2026, undisclosed), which I covered 2 weeks ago in The Food Stack. Across the Atlantic, Danone is actively pursuing Lifeway, the US kefir leader, with the company posting around $200M revenue and trading at high single-digit revenue multiples on the public market. The acquirer set is fully formed and actively buying.

The behavioural driver behind all of this is consistent. Consumers are pulling functional health into everyday food categories, and dairy is one of the cleanest places to express that. Kefir specifically benefits from a unique combination of advantages: it carries a recognisable health claim (live cultures and gut health), tastes familiar to consumers used to yoghurt drinks, sits at the same price point as premium yoghurt, and fits naturally into existing breakfast and snacking occasions. It does not require behaviour change. It is a small swap, not a lifestyle change, which is exactly the formula that wins in functional food today (a point Lisa Macfarlane made in my Gut Stuff piece two weeks ago).

For Müller specifically, the strategic logic is even sharper. Müller had previously launched its own kefir line (smoothies) in 2021 in the UK and discontinued it in 2023. The acquirer’s failed organic attempt is what made the deal economics work for Bowes. When an incumbent’s internal build does not succeed, the cheapest path to category presence is acquiring the leader. Müller’s offer reflected that. So did Bowes’s negotiating leverage.

A note on funding

There is no clean public funding history for Biotiful. PitchBook lists Tesco as an investor, but the underlying relationship is the 2019 Tesco Incubator Programme, which provides mentorship and retail relationships rather than equity capital in most cases. Tracxn says Biotiful raised no funding rounds at all. Crunchbase has the company listed but no investors. The Companies House filing also shows no SH01 filings consistent with a venture round.

Kefir continued to be part of Bowes’ diet and health regime as she trained as a figure skater, competing for her country up until the age of 13

What I can piece together from primary sources is that Biotiful was almost entirely founder-funded for 13 years. Bowes self-funded the early production phase from her finance career savings (KPMG, then Barclays Capital, both in the credit and risk side), making the first production-quality drinks herself in a small organic dairy in West Sussex during the founding year. The cap table appears to have been Bowes plus a handful of small individual minority holders (Natalia Levin, Kevin Moore, Rachel Phillips, and a holding entity called Kefir Limited, all visible in earlier confirmation statements).

That structure was tidy enough for Bowes to consolidate cleanly when the time came.

On 24 April 2024, almost exactly 12 months before the Müller deal, Biotiful executed a £4M share buyback that left Bowes as the sole shareholder of the company.

The buyback ended with Bowes holding 100% control of a business that would sell for £115M roughly 350 days later.

This sequence is significant. Buying out minority holders before a strategic exit is a classic founder move when you know the deal is coming. It increases the founder’s take of the proceeds, simplifies the negotiation, and ensures the acquirer is buying a clean cap table. At a £115M deal value with full ownership at exit, the proceeds to Bowes net of the £4M buyback are approximately £111M. That is one of the cleanest founder outcomes in (UK) CPG in recent memory, and it is the result of a decade of avoided dilution.

The Winner’s Playbook and Timeline

13 years. Approximately zero outside equity capital. £115M exit. The most striking thing about reading through the Biotiful story is how few major strategic decisions there actually were. Bowes did the same thing for 13 years, with discipline. This section walks through the timeline first, then the seven decisions that made the outcome possible.

The timeline

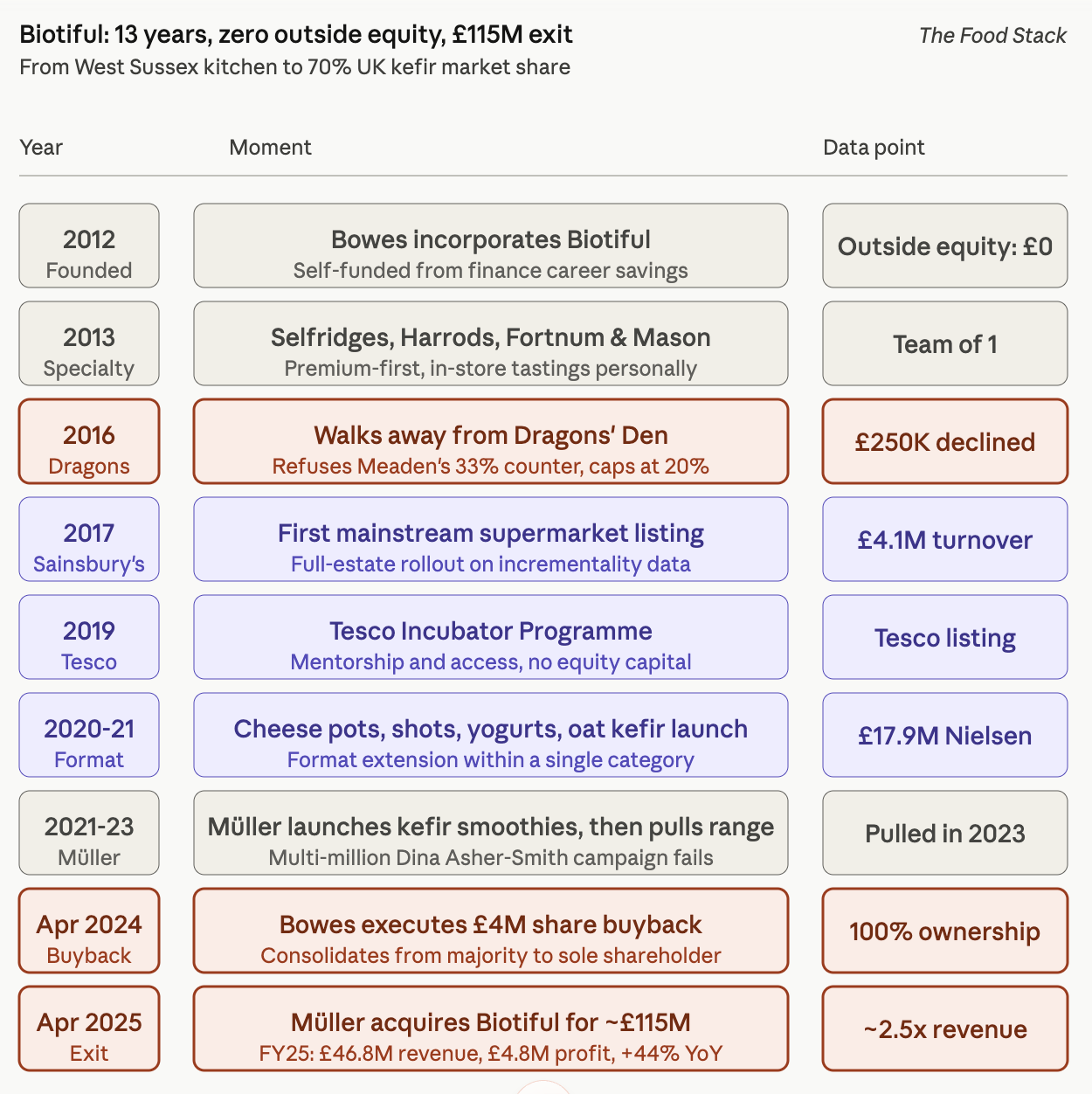

2012: Bowes incorporates Biotiful Dairy Limited. Self-funded from her finance career savings (KPMG, Barclays Capital). Spends the first nine months making the first production-quality drinks herself in a small organic dairy in West Sussex, with a consultant helping on technique.

2013-2015: First stockists are Selfridges, Harrods, and Fortnum & Mason. In-store tastings done personally to gather direct consumer feedback. Bowes works alone for nearly three years.

2016: Walks into Dragons’ Den asking for £250K at 10% (£2.5M valuation). Four Dragons walk away. Deborah Meaden offers the full £250K but demands 33%. Bowes caps her counter at 20% and leaves with nothing. Peter Jones calls her “uninvestable.” Meaden calls the valuation “crazy.”

2017: Sainsbury’s becomes the first major UK supermarket to list Biotiful. Rolls out to the full estate within six months on incrementality data. Revenue ~£5M.

2019: Selected for the Tesco Incubator Programme. Mentorship and buying-team access, not equity capital. Revenue ~£15M.

2020-2021: Aggressive format extension. Spreadable kefir cheese pots, shots, full-sized yoghurt pots, and the plant-based oat kefir line. Nielsen retail sales reach £17.9M in 2020.

2021-2023: Müller launches a UK kefir smoothie range with a multimillion-pound marketing campaign featuring Dina Asher-Smith as brand ambassador. Distribution across Tesco, Sainsbury’s, Asda, and Morrisons. Two years later, the range is discontinued.

In the same year, Biotiful launches a dedicateds kids kefir range.

April 2024: Biotiful executes a £4M share buyback. Bowes consolidates from majority shareholder to sole shareholder. Companies House filings (SH03 Purchase of Own Shares, SH06 Cancellation of Shares) confirm 100% ownership.

In the same year, Biotiful launched their first ever ambient Gut Health products.

FY25 (year to 31 March 2025): Revenue hits £46.8M, up 44%. Pre-tax profit reaches £4.8M, up 111%. Gross margin at 43%, up from 38% five years earlier. Tesco doubles its Biotiful range and launches a dedicated kefir bay. Aldi adds a Biotiful-produced own-label line.

April 2025: Müller acquires Biotiful for an estimated £115M. Richard Williams (CEO of Müller Yogurt & Desserts) joins the Biotiful leadership team. Bowes stays in an advisory capacity through the transition.

The seven decisions

Underneath the chronological story sit seven strategic decisions. Each one was a choice made differently than most UK CPG founders would have made it.

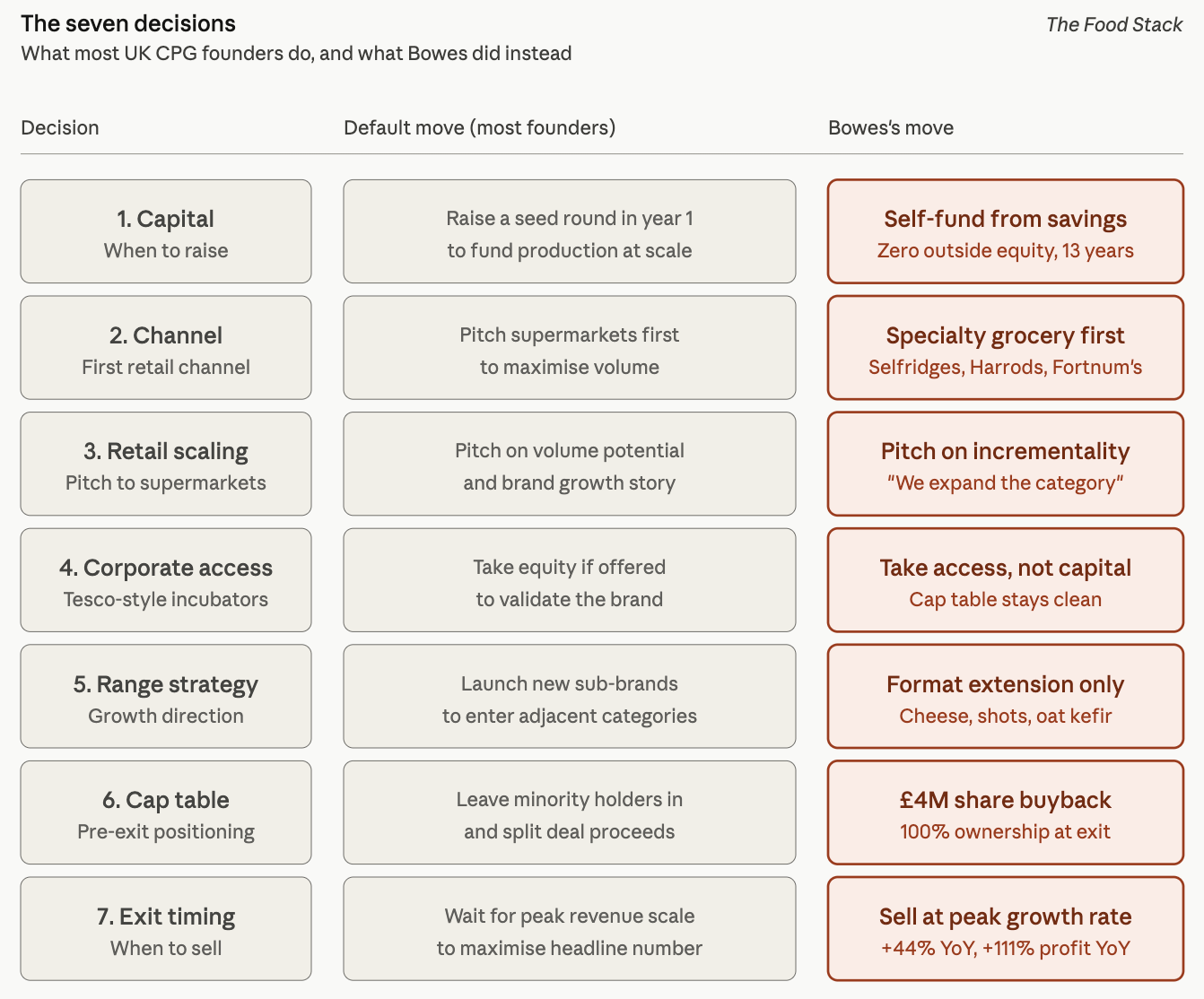

Decision 1: Bootstrap, and hold the line on valuation. Bowes did not raise outside equity capital across 13 years of building Biotiful. The most visible test of that discipline came at Dragons' Den in January 2016. Four of the five Dragons declined to invest. Deborah Meaden countered with £250K for 45% equity. Bowes capped her counter at 20% and walked away with nothing. The bootstrap discipline preserved her cap table for an exit she could not yet see. The lesson: bootstrap is not about avoiding capital. It is about avoiding the wrong kind of capital at the wrong moment, and holding the line on valuation even when an offer is on the table.

Bowes at Dragons Den in 2016

Decision 2: Specialty grocery first, mainstream retail second. Selfridges, Harrods, and Fortnum & Mason before any supermarket conversation. The lesson: the right early channel is the one where the consumer needs no education. Specialty grocery shoppers know what kefir is and accept higher price points.

Decision 3: Wait for incrementality before scaling retail. Sainsbury’s full-estate rollout in 2017 happened only after the brand could prove it was expanding the category rather than cannibalising existing dairy. The lesson: in a category with no shopper recognition, incrementality data is what unlocks supermarket-wide rollout.

Decision 4: Take corporate access, not corporate capital. The Tesco Incubator gave Biotiful mentorship and buying-team access without diluting the cap table. The lesson: corporate incubators provide real value when the value is access, not equity.

Decision 5: Format extension within a single category. Kefir cheese pots, shots, yoghurt pots, oat kefir. New SKUs compounded the existing brand equity rather than splintering into adjacent categories. The lesson: in a category with a strong founder brand, extending into adjacent formats is more capital-efficient than launching new brands.

I got the chance to talk to Natasha after publishing the article, which made me rewrite decision 6:

Decision 6: Consolidate the cap table, even when the timing feels risky. In April 2024, Bowes executed a £4M share buyback that left her as sole shareholder. She took on leverage to do it in a market that did not look favourable, which piled additional risk on her at exactly the wrong moment. The fact that Müller signed 12 months later was timing luck, not strategic sequencing. But the buyback created the cap table cleanliness that let her capture nearly all of the £115M outcome. The lesson: cap table consolidation is one of the highest-leverage moves a founder can make, even when it feels risky in the moment. The reason most founders never do it is precisely because the timing never feels right.

Decision 7: Sell at peak growth, not at peak revenue. A FY26 deal would have priced in a slowing growth curve. A FY24 deal would have missed the profit inflection. April 2025 was the optimum. The lesson: peak growth is when acquirers pay the highest multiple, not peak revenue.

One thing worth naming before the analysis goes further. Reading these seven decisions in sequence, it is tempting to conclude that Bowes operated from a deliberate 13-year playbook. She did not. When I shared an earlier draft with her, she pushed back on exactly that framing.

The reality, in her words, was passion, opportunism, grit, and timing luck.

The £4M buyback was nudged rather than planned, executed with leverage in a market that did not look good, and the fact that Müller signed 12 months later was timing rather than design. The seven decisions are real, but the sequencing is something the analyst sees in retrospect, not something the founder followed prospectively. That distinction matters. Business building does not always follow a formula. It follows a founder with conviction, instinct, and the willingness to make moves before the path is clear, with luck doing a meaningful share of the work. Extremely valuable, honest feedback. Thank you Natasha.

This is also one of the reasons why early-stage investors, including myself focus so much on the founders. We want to see someone who is obsessed, who has grit, who has “fire in the eyes”. It’s extremely important and Natasha just explained why.

Why Müller acquired Biotiful

Müller is buying the missing piece in its own UK functional dairy strategy.

Müller had tried to build kefir internally and failed. The cheapest path to a 70% market share position is to buy the brand that already holds it. The deal multiple (~2.5x revenue, ~24x pre-tax profit) reflects this structural logic. It is not a premium multiple by venture exit standards, but it is a clean strategic fit at a price both sides could justify.

Müller CEO Richard Williams said at the time:

“Biotiful Gut Health is a business we have long admired: it is one of the fastest growing brands in the sector, has great tasting products and a real focus on consumer and innovation. This is a business which fits really well within our existing portfolio of brands. We are already growing and optimising our range of health and nutrition products and Biotiful Gut Health will really help us expand into new growth areas to meet changing consumer needs.”

That language is measured. Williams is not framing the deal as transformational. He is framing it as fitting. Müller is buying capability it could not build internally, at a price that lets the integration be a steady margin contributor rather than a gamble.

How Others Are Playing It

Biotiful is not an isolated event. Three other deals tell the broader story.

The Collective, acquired by Yeo Valley in March 2025. Founded in New Zealand in 2008 and brought to the UK in 2011, The Collective was a private-equity-backed gourmet yoghurt and kefir brand with £26.6M turnover in FY24 (the year before the acquisition). Yeo Valley, a £750M-revenue family business that has been producing organic dairy in the UK since 1976, paid an undisclosed sum. The Collective’s post-deal accounts (published at Companies House) show revenue rising 16% to £31M in the 14 months to June 2025, with profits up from £362K to £1.3M. Yeo Valley CEO Rob Sexton framed the move as portfolio expansion into premium yoghurt and kids’ SKUs, not a gut health bet. Different acquirer, different rationale, lower multiple. The Collective sold for less than Biotiful despite a comparable revenue base, because Yeo Valley was buying portfolio diversification, not category leadership.

The structural lesson sits in the post-deal P&L. Yeo Valley’s group gross margins slipped from 14.1% to 13.6% in the year of the acquisition, and its long-term target of 5% pre-tax profit margin slipped further from 2.2% to 1.7%. I was really surprised when I read about these gross margins, they seem extremely low compared to ambient food and beverage brands (where 30-50% gross margins are standard) but they are typical for UK dairy producers who carry the full chilled supply chain on their books: volatile milk pricing, refrigerated logistics, short shelf life, and retailer pricing power.

Biotiful, by contrast, expanded gross margin from 38% to 43% over five years because it operates as a brand on top of a contract manufacturing relationship with First Milk rather than vertically integrated dairy production. The 25-30 gross margin point difference between Biotiful and Yeo Valley group is the structural reason brand-only functional dairy operators are attractive acquisition targets: the acquirer absorbs the brand into manufacturing it already runs at scale, and the brand’s gross margin profile improves the consolidated group’s product mix. This is the same logic Müller applied when acquiring Biotiful.

Lifeway Foods, the US kefir leader still resisting Danone’s acquisition attempts. Lifeway is a publicly listed Nasdaq company with FY25 revenue of $212.5M (up from $186.8M) and net income of $13.9M (up from $9M). Danone has owned approximately 23% of the stock since 2013 through a partnership agreement. The Smolyansky family controls another 30% on the founder side.

The pursuit started in September 2024, when Danone bid $283M ($25 per share). Two months later it raised to $307M ($27 per share). Lifeway’s board rejected both offers, calling them “opportunistic” at a multiple of 7-8.5x expected EBITDA. Danone sued in March 2025, alleging the Smolyansky family had improperly transferred shares between family members to consolidate voting control. Talks reopened under an NDA in August 2025, then collapsed in September. By October 2025, Danone had given up its board seat under a cooperation agreement and was reviewing options for its 23% stake. As of May 2026, the deal remains unclosed and Danone is widely expected to exit its position.

The pattern across the two comparators is consistent. Strategic acquirers in functional dairy are paying clean multiples for category leadership, founder-led discipline, and clean financial profiles. They are not paying premium multiples for revenue alone, and they will not pay any premium at all when the cap table is contested. Yeo Valley got The Collective at a discount because it was a portfolio play, not a category bet. Danone cannot close Lifeway because the cap table is contested even with 23% strategic ownership. Biotiful sits between the two: clean cap table, category leadership, strategic acquirer with a failed organic attempt behind it. That combination is what produces a premium multiple.

The deeper insight is who gets paid most. Biotiful at £46.8M revenue exits at ~£115M. The Collective at £26.6M exits at less than Biotiful despite a comparable revenue base. Lifeway at $212M cannot get a deal closed at all. Revenue scale is a poor predictor of exit value in functional dairy. Cap table cleanliness, founder control, and acquirer-specific strategic fit are the variables that actually determine the multiple.

What Went Wrong (or: The Risks)

This is the section I find most interesting to write because Biotiful is an unambiguous success, but the deal economics raise a question worth sitting with.

Why didn’t 70% market share command a richer multiple? At ~2.5x revenue, the Biotiful deal is a clean strategic exit but not a category-defining multiple. By comparison: Bachan’s exited at 4.6x revenue and Grüns at roughly 4-5x trailing revenue. What is happening is that kefir is structurally a lower-multiple category than ambient or premium-positioning consumer brands. Three reasons.

First, kefir is a chilled dairy product, which means it carries the supply chain economics of dairy. Margins are thinner than ambient categories because of cold chain logistics, shorter shelf life, and dependence on milk pricing volatility. Even with strong gross margins on the Biotiful brand specifically, the category ceiling on multiples is structurally lower than for shelf-stable functional brands.

Second, kefir is a defined category with a finite ceiling. Once the category reaches mainstream awareness (which it has in the UK), the growth shape changes. Biotiful grew 44% in FY25, while the category overall grew at “double digits”. The brand is taking share within a category that is itself maturing. Acquirers price this in. Category leadership in a maturing category is worth less than category leadership in an expanding one.

Third, the acquirer set is concentrated. Müller, Danone, and Lactalis are essentially the only large dairy groups with the manufacturing scale and distribution to absorb a brand at Biotiful’s volume. That concentration limits competitive bidding. A more fragmented acquirer set (as exists in functional snacking or beverages) would have produced a higher exit multiple. Bowes likely got the best price the market was willing to pay, but the market itself was constrained.

The second risk worth naming is the post-acquisition execution risk. Müller has not historically been an active acquirer of challenger brands. Biotiful’s success depended on agility (rapid product launches, direct relationships with retailers, clean ingredient positioning). Inside a CHF 1.5 billion conglomerate, that agility tends to slow. The brand’s continued growth under Müller will depend on whether the dairy giant can resist the temptation to integrate Biotiful too tightly into its own operational model. Williams’s measured language at deal announcement (”fits really well within our existing portfolio”) is reassuring, but reassurance is cheap at announcement. The next 24 months of execution matter.

The third risk is regulatory drift around health claims. EFSA’s regime on functional food claims is strict, and post-Brexit the UK regulatory framework has not diverged meaningfully. Biotiful has been disciplined about staying within approved live cultures language. Müller’s operating culture may not have the same restraint. Brands that overclaim get pulled. Brands that change positioning post-acquisition lose category authority. Both are risks worth watching.

Is There Room for New Entrants?

UK kefir is now structurally consolidated. Biotiful sits with Müller. The Collective sits with Yeo Valley. The remaining independent challengers (Bio&Me, Yeoboo, smaller regional players) are competing for the same shelf space against own-label products and the two major branded incumbents.

Continental Europe is a different story.

Three structural gaps stand out for European founders watching this category.

First, continental Europe has more functional dairy activity than the UK story suggests, but no single brand has yet built the category-defining position Biotiful holds in the UK. The category is dominated at the major brand level by five players. Danone leads with Activia, the world’s largest functional yoghurt brand, plus Actimel in the probiotic drinks segment. Lactalis, the world’s largest dairy company, holds a broad functional portfolio including Galbani and Siggi’s (acquired 2018). FrieslandCampina, the €11B+ Dutch cooperative, owns Vifit and Campina functional sub-brands across Northern Europe. Arla Foods carries the Nordic functional dairy position through its dominant Skyr range and kefir extensions. Yakult occupies the probiotic dairy shots subcategory almost alone at scale. Müller, now the owner of Biotiful, completes the major acquirer set. The challenger layer exists but is fragmented: Pastoret has built a credible premium kefir position in Spain since 1992 and exports across Europe, several Nordic skyr challengers (Isey, Smari) operate beneath the Arla canopy, and smaller regional players are scattered across most national markets. None has yet built the combination of category leadership share, multi-format extension, and premium positioning that Biotiful holds in UK kefir. The category-defining position at the European level is unclaimed.

Article published yesterday in Dutch newspapers about the huge rise in popularity for the “Skyr” brand in The Netherlands because of its high-protein / low-fat levels while still being creamy

Second, the EU functional food regulatory framework rewards brands that can prove substantiated health claims. EFSA-approved claims for live cultures and gut function exist but are tightly defined. A brand that leads with the approved claims (rather than aspirational marketing) has structural credibility that influencer-led brands cannot match. This is a defensibility lever, not a constraint. The same regulatory framework that makes life difficult for hype-driven US-style brands creates an opening for science-led European challengers.

Third, the strategic acquirer set is broader on the continent than in the UK. Danone, Lactalis, Bel, FrieslandCampina, and Arla are all active in functional dairy and all have active M&A pipelines. A continental European challenger brand that hits €30M to €50M revenue with strong unit economics has multiple credible exit paths, not just one. That competitive dynamic should produce higher multiples than the UK delivered for Biotiful.

There is one open question I do not have a confident answer to. Continental European supermarket structures are more fragmented than the UK’s. Listing in Carrefour does not translate automatically into Edeka or Mercadona. A category leader in one country may struggle to scale across borders even with strong product fundamentals. The brand that wins the continental opportunity will need to solve cross-border retail relationships in a way that Biotiful did not need to. That is a harder operational problem than building a single-country leader.

Honestly, I think this is one of the hardest categories to build in right now. Functional dairy in Europe is extraordinarily crowded. Danone, Lactalis, FrieslandCampina, Arla, and Yakult occupy the major positions, and the challenger layer is fragmented across dozens of regional players competing for the same shelf space. Any emerging winner will almost certainly have to do what Biotiful did: pick a niche format the incumbents are not building in, grow that niche into a category over a decade, and become the default brand by the time the category reaches mainstream awareness. That is the playbook. Kefir was an unknown product in the UK in 2012. Biotiful spent 13 years building both the brand and the category at the same time. Doing the same thing today in continental Europe requires identifying a format that is currently as unfamiliar as kefir was then, and most of the obvious candidates (skyr, viili, kvass, plant-based fermented drinks) already have credible challengers in market. The window is narrow.

That said, if I were placing the bet, I would look first at France or the Netherlands. Both markets have strong yoghurt drinking culture, smaller incumbents with limited challenger response, and proximity to the dairy supply chains that make scaled fermentation economically feasible. The brand that wins this will probably look something like Biotiful: founder-led, bootstrapped or lightly funded, anchored in a specific traditional fermented format (kefir, skyr, viili, or kvass-adjacent), launched through specialty grocery first, and built on a tight cap table. The exit, in 8 to 12 years, will probably be to Danone, Lactalis, or Müller again, for €100M to €300M.

I do not know which brand it is yet. If you are building it, my inbox is open, happy to talk.

Takeaways

The Müller acquisition of Biotiful Gut Health is the cleanest UK functional food deal of the past 18 months by data quality and the largest by absolute deal value. The story underneath is about founder discipline meeting a specific acquirer need at the right moment.

Biotiful was acquired by Müller in April 2025 for an estimated £115M on FY25 revenue of £46.8M (44% YoY growth, 33% 5-year CAGR) and pre-tax profit of £4.8M (111% YoY growth). Gross margin expanded from 38% to 43% over five years. Bowes executed under pressure in a difficult market, with timing luck doing meaningful work in the eventual outcome.

Müller’s 2021 attempt to build the kefir category internally failed and was discontinued in 2023. The deal economics worked because the acquirer had already proven that organic build was harder than acquisition. Future founders pursuing similar strategic exits should look for acquirers with publicly visible failed internal attempts in the target category.

Bootstrap discipline was worth approximately £49M in additional exit proceeds compared to a typical venture-funded path.

The deal multiple (~2.5x revenue, ~24x pre-tax profit) is clean but not extreme. Three structural factors explain the gap with 4-4.5x multiples we have seen in CPG before: dairy supply chain economics, category maturity, and a concentrated acquirer set. Future kefir exits will face the same ceiling.

A clean private cap table commands more pricing power than a public listing with a strategic anchor. Lifeway at $212M revenue cannot close a deal with Danone holding 23%. Biotiful at £46.8M revenue closed at roughly a 71% multiple premium over Lifeway’s public market valuation.

UK functional dairy is now structurally consolidated. The next opportunity is continental European, and the strategic acquirer set on the continent is broader than the UK’s.

If this was useful, share it with a founder or investor who would find it relevant, and leave a comment what topic you’d like me to dive in.

Bootstrap discipline is the right read. The trap is thinking any founder can do this.

Kefir produces 38 to 43% gross margin on contract-manufactured chilled dairy. No R&D cycle. No proprietary IP to defend. The category grew the brand for free once specialty grocery validated it. Bowes didn't refuse capital because she was disciplined. She refused it because her category didn't require it.

The diagnostic every founder should run before copying her: does my category produce margin and growth before product-market fit, or after? Before means you can bootstrap. After means capital isn't optional, it's structural. Get that wrong and you spend a decade underfunded in a category that needed money to exist.

Biotiful is a capital-structure case study, not a discipline case study.